#1 WRONG ASSET ALLOCATION

The top financial minds in the world differ in their strategies and approach to investing, but the common denominator is how they avoid making the following mistakes. Whether you are brand new to investing or you are a seasoned investor, you could be making these investment mistakes.

Anybody can become wealthy; asset allocation is how you stay wealthy.

Asset allocation is the most important investment decision of your life. It’s something that most investors may have heard of (or even fully understand) but know little about the practical application. Asset allocation protects you from a lack of diversification, from falling in love with one type of investment and not owning a variety of different types of assets.

However, asset allocation is more than just diversification. You may be diversified across asset classes or investment types, but are you also diversified across risk?

Asset allocation means dividing up your money among different investment classes (such as stocks, bonds, commodities, or real estate) in specific proportions that you decide in advance, according to your goals, needs, risk tolerance, and stage of life.

Yes, that’s a mouthful! Let’s walk through what that really means for you.

In order to create successful asset allocation think of it as your favorite sports team. The best teams have both an aggressive offense and a strong defense. And, most importantly, the coach knows the strengths and weaknesses of each. You want to set up a specific proportion of your portfolio as your tail end, or defensive position – we call this your Security or Peace of Mind bucket. In this bucket you will allocate lower risk assets, designed to protect you if your offensive players take a hit.

You will then set aside a specific portion of your money to be your offensive strategy – this is your Risk/Growth bucket. It is named this because although it will likely be the real wealth-growing portion of your portfolio, it is also the riskiest and most volatile.

Finally, you have a Dream bucket. This is for the really fun things you want in life. The dream vacations…the outrageous gifts… you fill in the blanks. You can fill this bucket by setting aside a proportion of your money like these other two or you can fill it when you have big wins – like a big bonus. This bucket isn’t meant to give you a financial payoff; it’s designed to give you a greater quality of life and keep you inspired to keep making your dreams a reality.

Because asset allocation is the most important investment decision you will make, it’s very likely that you’ll seek help in building that portfolio and filling those buckets. Take advantage of a free evaluation of the health of your own asset allocation and see how you compare to professionally designed portfolios. And when you do seek help, be sure not to make mistake number two.

#2 USING A BROKER INSTEAD OF A FIDUCIARY

You may have recently heard President Obama exhorting the Department of Labor to update their regulations of the financial industry and implement a fiduciary standard.

Why is the executive office concerned about the regulations of your broker? Because currently, brokers – also known as registered representatives, financial advisors, wealth advisors and more – are held to a “suitability standard” which does not require them to have their client’s best interests in mind. (Learn more about the fiduciary standard here.)

They oftentimes work for large, name-brand firms that are working only to make a profit. So, the person you turn to, although kind and trustworthy, is working in a closed-circuit environment, where the house it set up to win. A fiduciary, on the other hand, is independent and free of conflicts (or, at a minimum, they must disclose). A true fiduciary advisor never receives commissions to sell you a specific investment, or what you might call “having a dog in the fight.”

So what does it cost you to receive conflicted advice?

Using a broker instead of a fiduciary costs Americans one percent point of their return annually, according to The President’s Council of Economic Advisors. One percentage point may not sound like much, but one percentage point lower return could reduce your savings by more than a quarter over 35 years.

In other words, instead of a $10,000 retirement investment growing to more than $38,000 over those 35 years (after adjusting for inflation), it would be just over $27,500.

#3 INVESTING WITHOUT TAXES IN MIND

Insiders know that it’s not what you earn that matters, it’s what you keep. In fact, tax efficiency is one of the most direct pathways to shorten the time it takes to get from where you are now to where you want to be financially.

Did you know that the average American will pay more than half of his or her income to interest expense and taxes (income tax, property tax, sales tax, tax at the pump, etc.) over the course of their lives?

You can guarantee that this seriously impacts your ability to created compounded growth for your future life. There is no good reason to pay more in taxes than you have to, and every reason to avoid unnecessary taxes. Tax efficiency = faster financial freedom. Talk to your registered investment advisor, your CPA and utilize resources such as MONEY: MASTER THE GAME and this blog to discover 100% legal strategies for maximum tax efficiency.

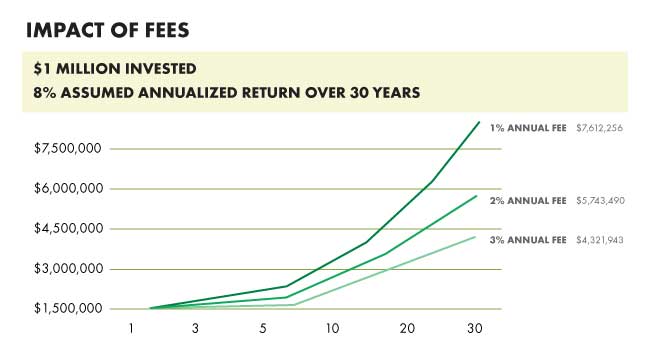

#4 OVERPAYING FOR HIGH-COST MUTUAL FUNDS

For years, we have been sold the lie that mutual funds are the most effective way to grow our 401(k)s. Unfortunately, it’s just not true. The truth is that 96% of actively managed mutual funds do not beat the market over a 15-year span. Active managers are trying to beat the market by being a great stock picker. And the 4% that does beat the market is changing all the time, so betting on a jockey that won the last race does not mean that he will win again. Chasing performance is a fool’s errand.

How badly does this actually hurt us? Over a 20-year period – December 31, 1993 through December 31, 2013 – the S&P 500 returned an average annual return of 9.28%. However, the average mutual fund investor made just over 2.54%, according to Dalbar, one of the leading industry research firms. That’s nearly an 80% difference!

To add insult to injury, the “all-in” cost of mutual funds is on average 3.17% per year, according to Forbes. This is when you add the management fees, the transaction costs, the sales loads, etc. Perhaps this number doesn’t sound high to you. Consider this: The market was “flat” between 2000 and 2009, a period known as the lost decade. There were lots of ups and downs, but nobody made money. If you were paying 3% annually during this period, your $100,000 portfolio would have approximately $70,000 (or be down 30%) at the end of this “flat” period.

You put up the capital, you took all the risk — and they made the money.

#5 FAILING TO DEVELOP THE DISCIPLINE OF REBALANCING

To be a successful investor, you need to rebalance your portfolio at regular intervals. This means you have to take a look at your buckets and make sure your asset allocations are still in the right ratio. From time to time, a particular part of one of your buckets may grow significantly and disproportionally to the rest of your portfolio and throw you out of balance.

Let’s say, for example, you start out with 60% of your money in your Risk/Growth bucket and 40% in your Security bucket. Six months later, you check your account balances and find out that your risk/growth investments have taken off and they no longer represent 60% of your total assets – it’s more like 75%. That means that only 25% of your money is safely in your security bucket. It’s time to rebalance!

The challenge with rebalancing is the emotional and psychological discipline it takes to actually do it. When a portion of your portfolio is doing really well, it’s easy to be hypnotized into the illusion that your current investment successes will continue forever, or that the current market can only go up. This is what causes people to stay with an investment too long and end up losing the very gains (and often more) that they were originally so proud of. The rules of rebalancing don’t guarantee you’re going to win every time. But rebalancing means you’re going to win more often.

How often do you need to rebalance? Most investors rebalance once or twice a year. Some rebalance more frequently, choosing to watch their portfolio more closely and adjusting when it starts to shift, but too frequently can hurt you as it doesn’t give a chance to “let your runners run.” The number of times you rebalance does have an impact on your taxes, however. If your investments are not in a tax-deferred environment, and you rebalance an asset you have owned less than a year, you’ll typically pay ordinary income taxes instead of the lower long-term investment tax rate.

Images copyright @connel/shutterstock, @Phase4Studios/shutterstock, @Anatoli-Styf/shutterstock

Team Tony

Team Tony cultivates, curates and shares Tony Robbins’ stories and core principles, to help others achieve an extraordinary life.

Source: https://www.tonyrobbins.com/wealth-lifestyle/5-costly-investing-mistakes/

No comments:

Post a Comment